State of the Capitol Region 2025

The Capital Region Post-COVID:

What Changed and What’s Next?

This report is a collaborative effort from researchers at the American Enterprise Institute, Georgetown University, and the George Washington University. We are particularly grateful to the Trachtenberg School of Public Policy and Public Administration and the George Washington Institute for Public Policy for their support. We very much appreciate the support of George Washington student Karolina Koletic, who expertly prepared our graphics.

Introduction

In this year’s State of the Capital Region, we explore how the pandemic has shifted people, employment and real estate prices across the region. In broad strokes, the sudden hit of the pandemic increased housing values in the Capitol Region’s exurban areas, and decreased housing values in urban areas. With the rise of remote work, employment shifted away from the urban core and out to exurban jurisdictions.

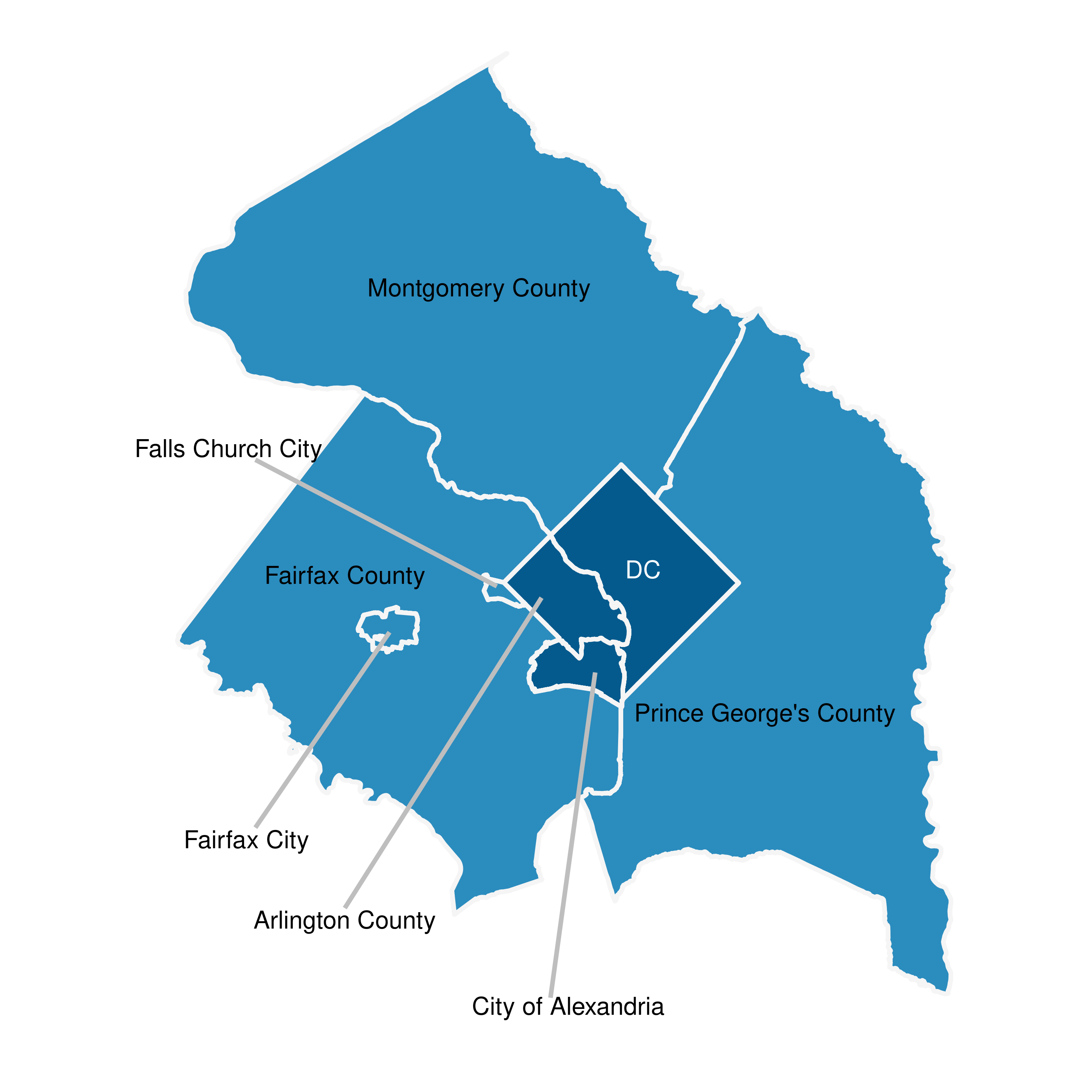

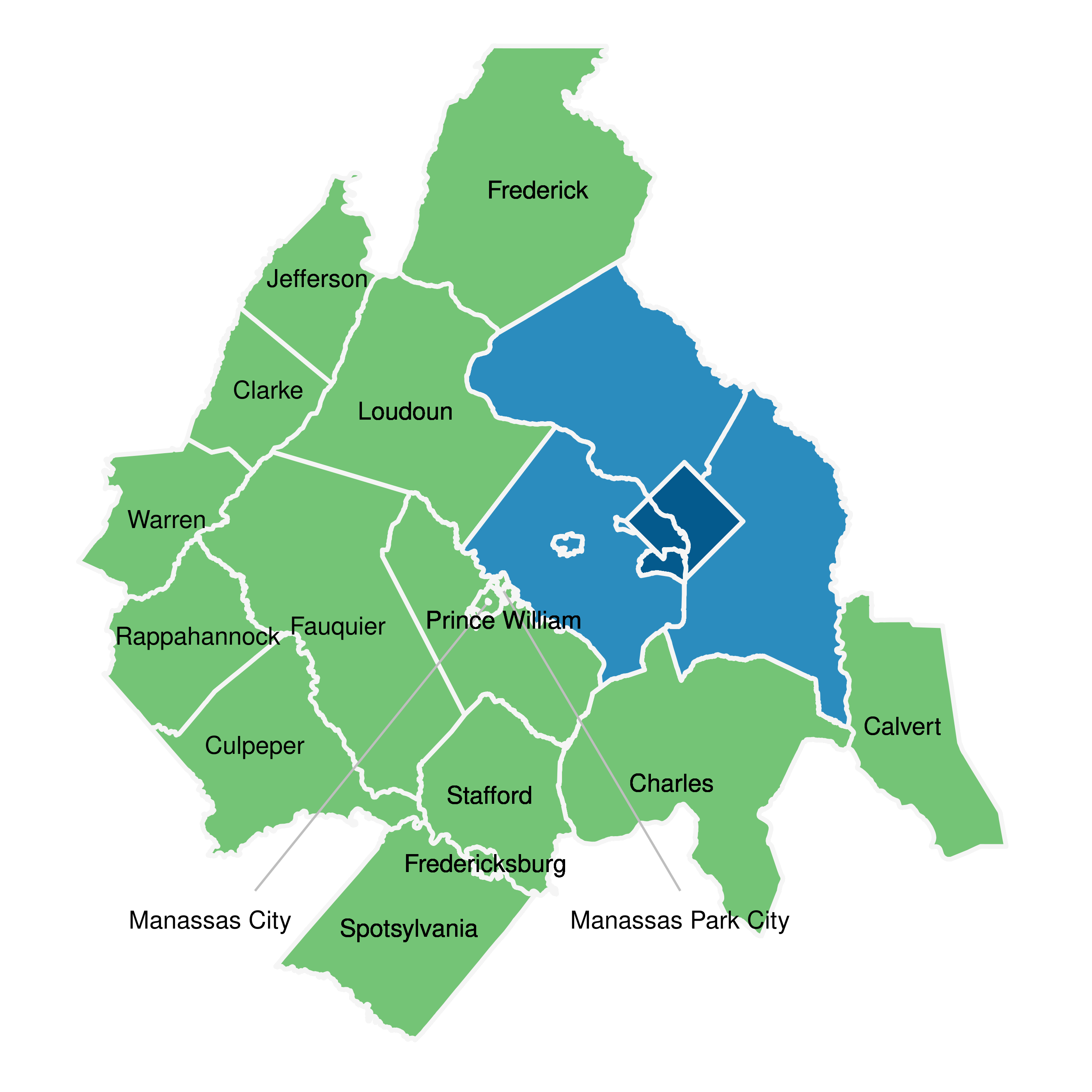

Figure I.1 below shows urban areas in dark blue – the District, Alexandria and Arlington – and suburban areas in light blue, defined as the older surrounding jurisdictions. We show exurban jurisdictions in green, the most populous of which is Loudoun County.

Figure I.1: Jurisdictions of the Capital Region

Urban, Suburban, and Exurban Jurisdictions of the Capital Region

Notes: Figure I.1 shows the urban jurisdictions in dark blue, the suburban jurisdictions in light blue and exurban jurisdictions in green.

Sources: Census Bureau, 2010 jurisdictional boundaries.

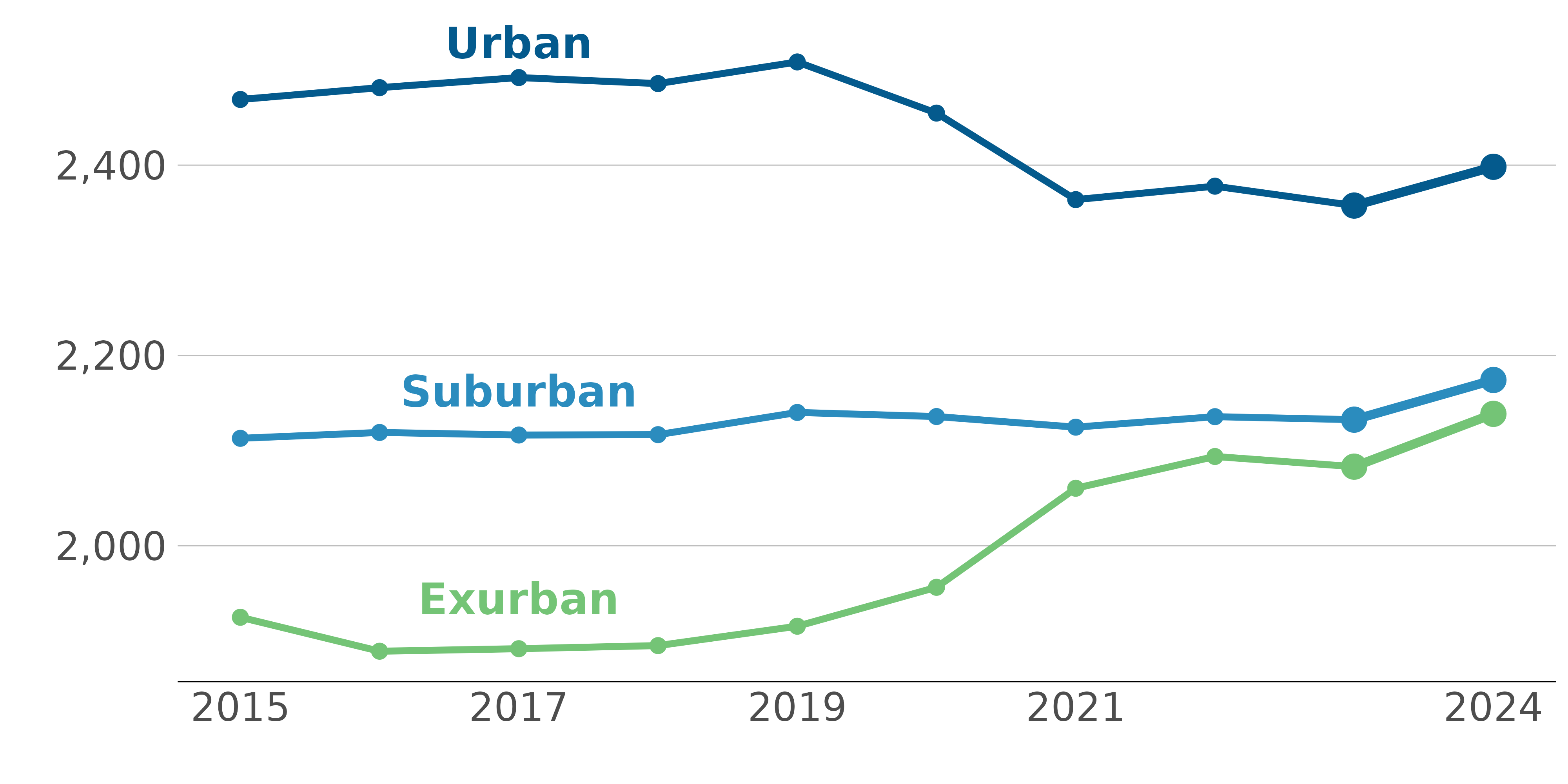

After the big hit of the pandemic, employment and real estate values farther from the urban area softened somewhat. Figure I.2 shows residential rent in urban, suburban, and exurban areas. In the 4 years following the pandemic, rent decreased by 4 percent in urban areas, and increased by 12 percent in exurban ones. But this difference moderated as rent increased from 2023 to 2024 in all parts of the Capital Region. Chapter 1 discusses rent patterns, and examines how commercial real estate has fared across the region.

Figure I.2: COVID Causes Rent Divergence, Easing of Pandemic Shows Rent Convergence

Average monthly rent for a housing unit in urban, suburban, and exurban jurisdictions, 2015-2024, 2024 dollars

Notes: Rent by area type from 2015-2024. We remove Manassas City, Falls Church City, Manassas Park City, and Fairfax City. These jurisdictions have no data before 2019. Housing unit weighted average rent in USD for urban, suburban, and exurban jurisdictions. Used inflation adjustment for 2024 through August only.

Sources: Zillow Research: Zillow Observed Rent Index, by county (or Virginia independent city) by year.

These real estate trends generally mirror trends in population (Chapter 2) and employment (Chapter 3). In Chapter 2, we show how population has reorganized across the Capitol Region and how urban areas lost population during the pandemic, but gained households. In Chapter 3, we document the sharp rise in remote work, and related declines in hospitality employment. We show how hospitality employment has largely recovered from its pandemic drop in exurban areas, but still lags pre-pandemic levels in urban and suburban areas.

With the arrival of the Trump Administration, the region is facing more changes. The return to office mandates for federal workers should tend to return the distribution of population to its pre-pandemic pattern across the Capital Region. This should convey a knock-on effect to retail real estate, which will benefit from greater foot traffic.

In contrast, shrinking the federal workforce may decrease employment, at least in the short term, across the Capitol Region, and likely most sharply in the urban area. This should work to decrease residential real estate prices and the value of retail real estate. Federal lease cancellations should also work to lower prices in the regional office market. In the long run, this office space may be reallocated to residential use. Creating new residential units could be a boon to affordability in the region by reducing rents without reducing residential demand.

Thus, conditions in the Capital Region are in flux. While the impacts of the pandemic seem to be fading away, the area is facing new challenges. Some of these new challenges have short-run costs, and potential long-run rewards. In the short run, reallocation of land uses or job locations may be painful and costly. In the long run, the creation of more housing units, or a workforce better prepared to meet new digital challenges may be a source of strength for the region.